“The Ultimate Budget Planner: Simple Strategies to Track Income, Expenses & Save More”

“The Ultimate Budget Planner: Simple Strategies to Track Income, Expenses & Save More”

Easy Budget Planner: Balancing Your Income and Expenses Effectively

Introduction Managing personal finances is crucial for financial stability and success. A well-structured budget planner helps track income, expenses, and savings to ensure a balanced financial life. In this comprehensive guide, we will explore how to create an easy budget planner, manage income and expenses effectively, and maintain financial balance.

What is a Budget Planner?

A budget planner is a financial tool that helps individuals and households manage their income, expenses, and savings. It allows users to allocate funds to different categories and track financial progress over time.

Why Use a Budget Planner?

- Financial Awareness: Keeps track of where your money goes.

- Prevents Overspending: Helps set spending limits.

- Encourages Savings: Ensures money is set aside for future needs.

- Debt Management: Assists in paying off loans efficiently.

- Goal Setting: Helps achieve financial milestones like buying a house or retirement planning.

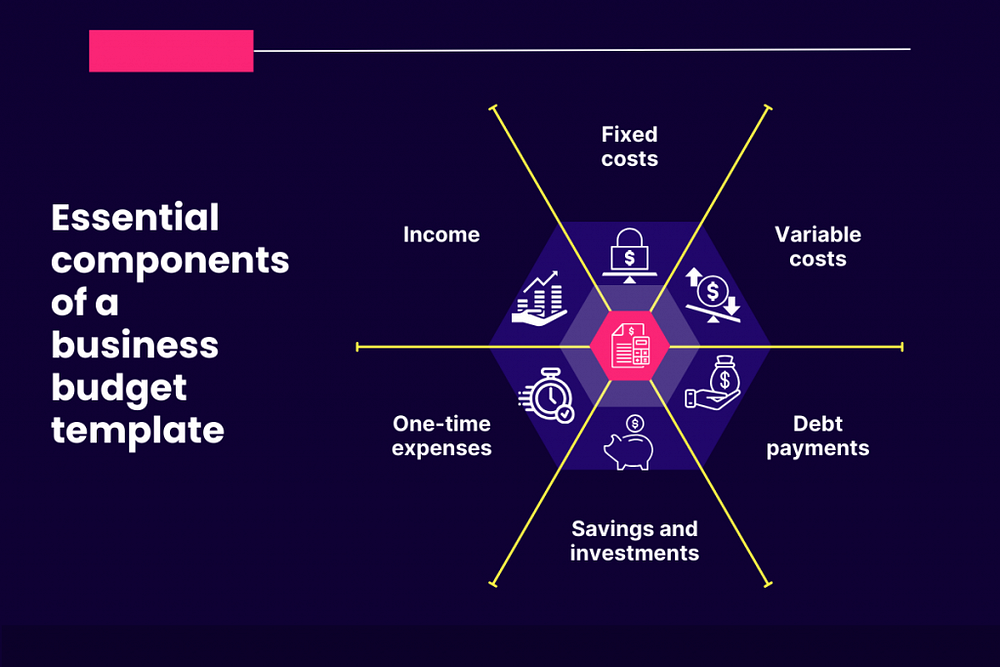

Essential Components of a Budget Planner

1. Income Tracking

- Primary Salary

- Side Hustles

- Rental Income

- Investments and Dividends

2. Fixed Expenses

- Rent or Mortgage

- Utilities (Electricity, Water, Gas, Internet)

- Insurance (Health, Home, Car)

- Loan Payments

- Subscriptions (Streaming Services, Gym Memberships)

3. Variable Expenses

- Groceries

- Dining Out

- Transportation

- Entertainment

- Shopping

4. Savings and Investments

- Emergency Fund

- Retirement Savings

- Stock and Bonds Investments

- Real Estate Investments

- Education Fund

5. Debt Management

- Credit Card Payments

- Personal Loans

- Student Loans

Steps to Create an Easy Budget Planner

Step 1: Calculate Your Total Income

List all sources of income to determine your total available funds each month.

Step 2: List Your Monthly Expenses

Categorize expenses into fixed and variable to identify necessary and flexible costs.

Step 3: Set Financial Goals

Decide on short-term and long-term financial goals, such as saving for a vacation or paying off a mortgage.

Step 4: Allocate Your Budget

Use the 50/30/20 rule as a guideline:

- 50% for necessities (rent, utilities, groceries)

- 30% for wants (entertainment, shopping, dining out)

- 20% for savings and debt repayment

Step 5: Track and Adjust Spending

Regularly review your budget and make adjustments to improve financial efficiency.

Step 6: Automate Payments and Savings

Set up automatic bill payments and transfers to savings accounts to avoid missed payments.

Best Tools for Budget Planning

1. Budgeting Apps

- Mint

- YNAB (You Need a Budget)

- PocketGuard

- GoodBudget

2. Spreadsheet Templates

- Microsoft Excel Budget Template

- Google Sheets Budget Planner

3. Budgeting Journals

- Physical planners for those who prefer manual tracking.

Balancing Income and Expenses

1. Increase Income

- Take on Freelance Work

- Invest in Stocks or Real Estate

- Start a Side Business

- Rent Out Unused Space

2. Reduce Expenses

- Cut Unnecessary Subscriptions

- Cook at Home Instead of Eating Out

- Use Public Transport Instead of Driving

- Shop During Sales and Use Coupons

3. Build an Emergency Fund

- Aim to save at least 3–6 months’ worth of expenses for unexpected situations.

4. Avoid Unnecessary Debt

- Use Credit Cards Wisely

- Pay Off High-Interest Loans First

Common Budgeting Mistakes to Avoid

- Underestimating Expenses

- Not Tracking Small Purchases

- Failing to Adjust the Budget When Income Changes

- Over-Reliance on Credit Cards

Conclusion

A well-structured budget planner is essential for financial success. By tracking income and expenses, setting realistic goals, and making informed financial decisions, you can achieve stability and financial freedom. Start budgeting today and take control of your finances!

Comments

Post a Comment